TENNANT (TNC)·Q4 2025 Earnings Summary

Tennant Crashes 72% Below EPS Estimates as ERP Disaster Derails Quarter

February 24, 2026 · by Fintool AI Agent

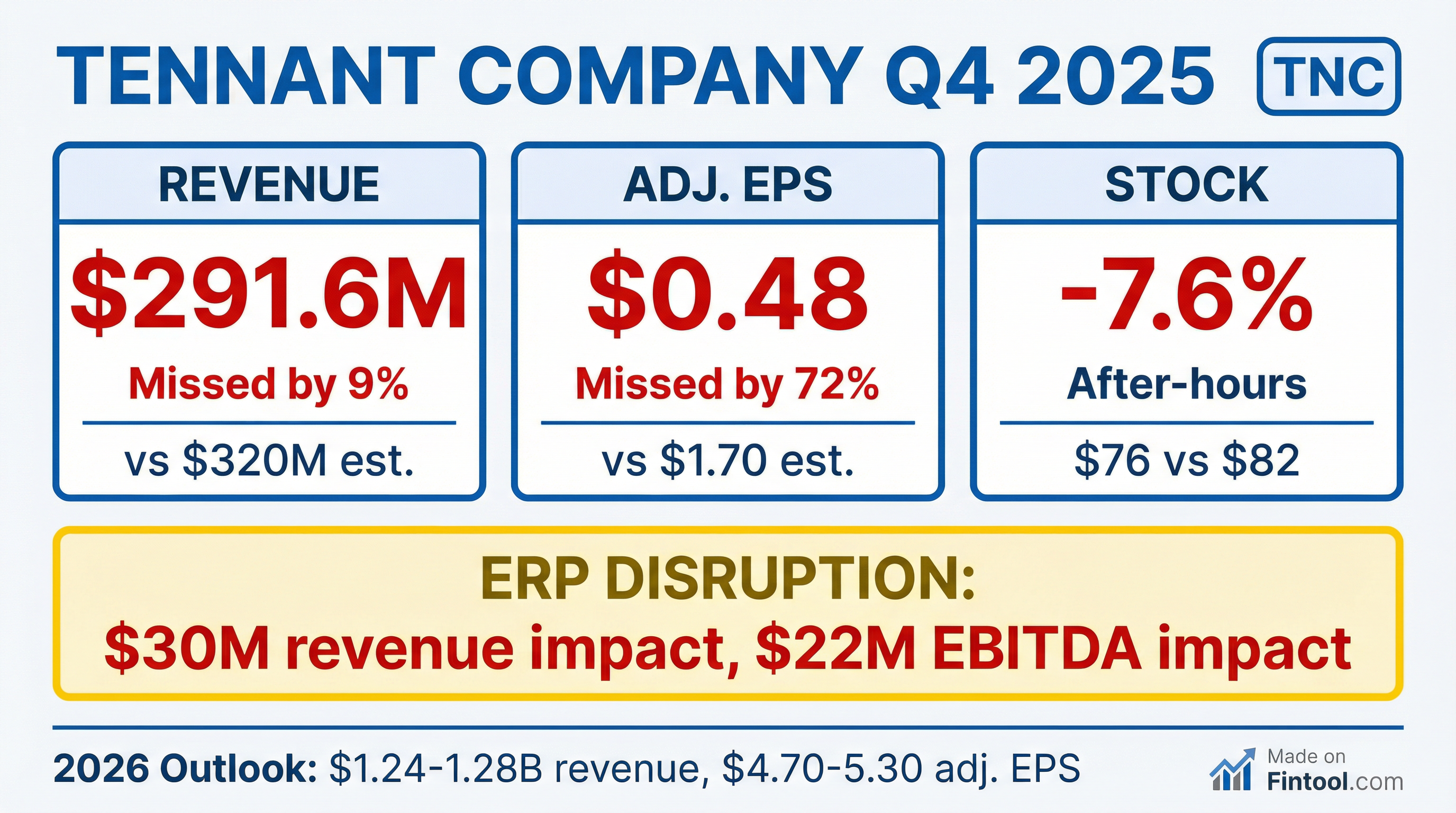

Tennant Company (NYSE: TNC) reported a disastrous Q4 2025 as an ERP system implementation in North America caused severe operational disruptions. Adjusted EPS of $0.48 missed consensus by 72%, while revenue of $291.6M missed by 9% . The stock fell 7.6% in after-hours trading to $76.06.

Did Tennant Beat Earnings?

No — this was a catastrophic miss on both revenue and earnings:

For the full year 2025, Tennant delivered revenue of $1,203.5M (vs. $1,232.4M expected) and adjusted EPS of $4.57 (vs. $5.77 expected), missing guidance on both metrics .

What Caused the Miss?

The culprit is clear: Tennant went live with a new ERP system in North America in the first week of November 2025, and the transition introduced "unexpected challenges" that constrained operating capacity :

- Order management and fulfillment disruptions

- Manufacturing scheduling issues and reduced inventory visibility

- Slower transaction processing and prolonged customer delays

Management estimates the ERP disruption cost approximately:

- $30 million in lost net sales

- $22 million in adjusted EBITDA

- $0.91 per share in EPS impact

ERP Program Costs: Total investment since 2023 is ~$98 million. The 2026 ERP-related spending is now expected to exceed $20 million — up from the $5 million originally planned — to complete remediation and maintain hypercare support . EMEA go-live has been paused indefinitely to focus on North America recovery .

"Despite a successful go-live in the APAC region in September and extensive preparation in North America, the cut-over of the ERP system in the first week of November introduced severe system functionality issues that limited our ability to enter orders, ship products, and service our customers." — Dave Huml, CEO

Gross profit margin collapsed to 34.6% from 41.3% in Q4 2024, driven by the ERP transition effects including an estimated $13.5M volume impact and ~$8.5M of incremental costs .

How Did the Stock React?

TNC closed at $82.30 on February 23, 2026, down 1.2% in regular trading. After the earnings release, the stock plunged to $76.06 in after-hours trading — a 7.6% decline.

The magnitude of the miss explains the reaction. A 72% EPS miss is extreme by any standard, even accounting for the ERP disruption context. Investors are now pricing in continued uncertainty through H1 2026.

What Changed From Last Quarter?

The sequential deterioration is stark. Gross margin dropped 810 basis points in a single quarter — nearly all attributable to the ERP transition that went live in early November.

Beat/Miss Track Record (Last 8 Quarters):

Values retrieved from S&P Global

Tennant had been a reliable beat machine through 2024 but has now missed three of the last four quarters, with Q4 2025 being the worst by far.

What Did Management Guide?

For 2026, Tennant provided guidance that implies a recovery, though Q1 will remain challenged :

Critical context: Management expects Q1 2026 to remain depressed:

- A two-week manufacturing shutdown in early January 2026 for physical inventory will significantly affect Q1 sales

- Q1 margins expected to be "comparable to Q4 2025" before improving sequentially

- Normalization expected by mid-2026, with significant improvement in the second half

What's the Margin Trajectory?

Margins have been under severe pressure:

Gross margin had been relatively stable in the 41-44% range until the ERP disaster. The 34.6% Q4 print represents a multi-year low.

Beyond ERP, tariff-related material cost pressures also contributed to margin compression .

Regional Performance

Geographic results varied significantly :

The Americas bore the brunt of the ERP disruption since the system went live in North America. EMEA and APAC showed relative resilience, with APAC posting double-digit Q4 growth driven by Australia, China, South Korea, and India .

TNC Robotics: The Growth Catalyst

A major bright spot: Tennant launched a dedicated TNC Robotics organization to accelerate its autonomous mobile robot (AMR) business :

CEO Dave Huml on the strategic rationale:

"We see this as both an opportunity and maybe a potential threat from these upstart robotics-only competitors... We decided in concert with our board to make a bold move, to make a step change investment and face off differentially to accelerate our growth in robotics." — Dave Huml, CEO

Key AMR Initiatives:

- Accelerating NPD roadmap to bring products to market faster

- Improving deployment and adoption efficiency

- Expanding demand generation to reach more customers via distribution

- Demonstrating ROI through machine data and KPI tracking

Management acknowledged pricing pressure from Asian robotics-only competitors who are "very fast, very agile" and gaining distribution positions .

Capital Allocation and Balance Sheet

Despite the operational challenges, Tennant's balance sheet remains solid :

- Cash: $106.4M at year-end

- Unused credit facility: $374.3M

- Net leverage: 1.0x Adjusted EBITDA (within 1x-2x target)

- Share repurchases: ~$88.5M in 2025 (about 6% of shares)

- Dividends: $21.9M paid in 2025

- ERP investment: $59.1M total in 2025 ($30.6M capitalized)

Free cash flow was $43.3M in 2025, or $102.4M excluding ERP spend — representing 157% conversion of net income when excluding ERP costs .

Q&A Highlights

On ERP System Stability (Tom Hayes, Roth Capital):

"We're stable in terms of our big five processes. You know, as a manufacturing business, we've got to be able to book orders, build, ship, invoice, and collect, and we are capable of transacting across that range of capabilities... If in comparison to what we experienced in the first three weeks of November, where we were unable to enter orders in the system, yes, I would say we are far more stable." — Dave Huml, CEO

On Customer Loss Risk (Steve Ferazani, Sidoti):

Management acknowledged customer frustration but indicated most relationships remain intact:

"Largely speaking, we're still in contact with all of our customers. Where we've lost business, it's customers and distributors that told us we were gonna lose it... The vast majority of our customers, and certainly the largest, are in that first camp, where they're frustrated... We're working with them." — Dave Huml, CEO

Huml noted that customer frustration doesn't correlate directly with revenue — a $100 parts order for a downed machine creates more urgency than a $50,000 equipment order with lead time .

On AMR Pricing Pressure (Aaron Reed, Northcoast Research):

"We are seeing pricing pressure from our competitors, all of our competitors, but I would say especially the upstart robotics-only competitors. These are brand-new, upstart companies. They don't have an embedded business they're trying to protect... That's another one of the reasons we decided to stand up the TNC Robotics venture." — Dave Huml, CEO

On Share Buybacks:

Management signaled continued aggressive buybacks given the attractive valuation:

"We've said before on publicly, as we look out... if we don't have a strategic M&A opportunity of size that's imminent, and the stock is at an attractive price, then we're gonna participate in buybacks... Don't be surprised if we start flexing that here, especially if the stock reacts negatively to our ERP challenges." — Dave Huml, CEO

Board Changes: VisionOne Settlement

Tennant announced board changes following engagement with activist investor VisionOne :

- Two new directors: James Glerum (Tennant nominee) and Patrick Allen (VisionOne nominee)

- Cooperation agreement with customary standstill provisions

- Declassified board: Moving away from staggered board starting 2027

What to Watch Going Forward

Near-term catalysts:

- Q1 2026 results — will reveal whether ERP stabilization is on track or if problems persist

- Mid-year operational update — management's target for normalized operations

- Tariff developments — additional cost pressures being managed through pricing

Key risks:

- ERP recovery takes longer than expected

- Customer attrition from Q4 fulfillment issues

- Tariff uncertainty — guidance was formulated before last week's Supreme Court ruling on tariffs; management will need to assess the impact

- North America industrial demand remains soft

Positive signals to watch:

- Orders grew ~4% in 2025

- Backlog increased ~$15 million

- Core processes improving per management

The Bottom Line

Tennant's Q4 2025 was a disaster driven almost entirely by a botched ERP implementation. The 72% EPS miss and 9% revenue miss rank among the worst quarters in company history. However, this appears to be a self-inflicted operational wound rather than a fundamental business deterioration — orders and backlog are growing, and international markets performed well.

The key question is execution: Can management stabilize the new system and return to normalized operations by mid-2026? The 2026 guidance implies they can, but investors will need to see proof in Q1 results. Until then, expect continued volatility around a stock that has now traded from $88+ highs to $76 in after-hours trading — a 14% drawdown from 52-week highs.

This analysis was generated by Fintool AI Agent on February 24, 2026. View the full earnings documents or explore Tennant's company page.